Every parent wants to secure their child’s future, especially when it comes to education and long-term financial stability. With education costs rising faster than inflation, traditional savings options like fixed deposits or recurring deposits may not be enough.

This is why many parents today are learning how to invest in direct mutual funds for your child.

The challenge is that most investment advice makes things unnecessarily complex — too many funds, confusing strategies, and constant monitoring. The truth is, investing in direct mutual funds for your child does not need to be complicated at all.

In this detailed guide, you’ll learn how to invest in direct mutual funds for your child without overcomplicating it, using a clear, simple, and long-term approach suitable for Indian parents.

Why You Should Start Investing for Your Child Early

Before understanding how to invest in direct mutual funds for your child, it’s important to understand why starting early matters.

Benefits of Early Investing

- Longer investment horizon allows compounding to work powerfully

- Lower monthly investment required

- Ability to take controlled equity exposure

- Reduced financial stress in later years

For example, starting when your child is 2 years old instead of 10 years old can reduce your required monthly SIP by almost half for the same goal.

Why Direct Mutual Funds Are Ideal for Child Investments

When planning a child mutual fund investment, choosing direct plans makes a significant difference.

Advantages of Direct Mutual Funds

- Lower expense ratio compared to regular plans

- No distributor or agent commission

- Higher long-term returns due to cost savings

- Complete transparency and control

Since child-related goals are typically long-term (10–18 years), even a small difference in expense ratio can create a large difference in final corpus.

This is one of the biggest reasons parents prefer learning how to invest in direct mutual funds for your child instead of regular plans.

Why Direct Mutual Funds Are Recommended by Regulators and Experts

When parents research how to invest in direct mutual funds for your child, it’s important to rely on data-backed guidance rather than opinions.

According to the Association of Mutual Funds in India (AMFI), direct mutual fund plans have a lower expense ratio compared to regular plans, which directly improves long-term returns for investors.

Who Can Invest in Mutual Funds for a Child?

You can invest if:

- The child is below 18 years of age

- You are a parent or legal guardian

- You have valid PAN and KYC

- You can commit to long-term investing

Any parent planning education, marriage, or future financial independence should consider direct mutual funds for child investments.

Step-by-Step Guide: How to Invest in Direct Mutual Funds for Your Child

Step 1: Open a Minor Mutual Fund Account

To begin direct mutual fund investment for your child, you need a minor account.

Documents Required

- Child’s birth certificate

- Child’s PAN card (mandatory)

- Parent/guardian PAN & KYC

- Bank account in child’s name or joint account

The parent acts as the guardian and manages the investment until the child turns 18.

Step 2: Choose a Platform That Offers Direct Mutual Funds

When learning how to invest in direct mutual funds for your child, always use direct investment platforms.

You can invest through:

- AMC official websites

- Direct-only investment platforms

- Reputed brokers offering only direct plans

Popular and trusted options include:

- ICICI Prudential Mutual Fund website

- Zerodha Coin (direct mutual funds only)

- AMFI-backed awareness platform Mutual Funds Sahi Hai

These platforms allow paperless account opening and SIP setup.

Step 3: Select the Right Mutual Funds (Keep It Simple)

This is where most parents overcomplicate their child mutual fund investment.

Simple & Effective Fund Structure

- One index fund or large-cap fund for stability

- One flexi-cap or diversified equity fund for growth

- Optional hybrid fund if you prefer lower volatility

❌ Avoid:

- Too many funds

- Sectoral or thematic funds

- Frequent switching

Simplicity is the key when deciding how to invest in direct mutual funds for your child.

SIP vs Lump Sum: What Works Better for Child Investments?

For most parents, SIP is the best way to implement direct mutual funds for child goals.

Why SIP Is Better

- Encourages disciplined investing

- Reduces timing risk

- Uses rupee cost averaging

- Easy to increase via step-up SIP

Even a SIP of ₹3,000–₹5,000 per month can grow into a sizable corpus over 15–18 years.

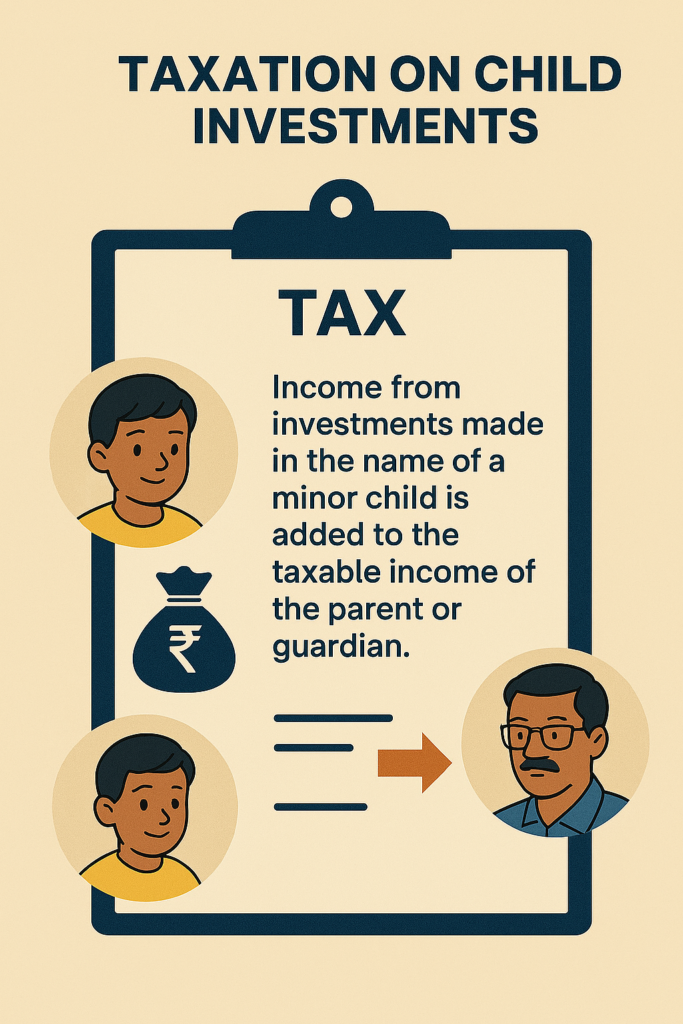

Tax Rules You Must Know Before Investing

Understanding tax rules is essential when learning how to invest in direct mutual funds for your child.

Taxation Explained Simply

- Income from child’s investment is clubbed with parent’s income

- Equity mutual funds:

- LTCG above ₹1 lakh is taxable

- STCG taxed as per rules

- Debt mutual funds taxed as per holding period

Choosing the earning parent as guardian is usually more tax-efficient.

What Happens When the Child Turns 18?

Once the child becomes a major:

- KYC must be completed in the child’s name

- Guardian status is removed

- Investment ownership shifts to the child

Planning this transition early ensures a smooth continuation of investments.

Common Mistakes Parents Should Avoid

While learning how to invest in direct mutual funds for your child, avoid these common mistakes:

- Over-diversification

- Chasing high-return funds

- Stopping SIPs during market downturns

- Mixing child investments with personal goals

- Monitoring investments too frequently

Long-term investing rewards patience, not panic.

How Often Should You Review Child Mutual Fund Investments?

You don’t need constant tracking.

Best Practice

- Review once a year

- Increase SIP with income growth

- Rebalance only if fund performance is consistently poor

This keeps direct mutual fund investment for your child stress-free and effective.

Important SEO Truth: About Linking to ICICI, Zerodha & Mutual Funds Sahi Hai

❌ Myth

Linking to top websites automatically improves rankings.

✅ Reality

Linking to high-authority, relevant websites:

- Improves topical relevance

- Increases trust (E-E-A-T)

- Helps users verify information

It supports SEO, but rankings still depend on content quality, structure, and user engagement.

So yes — linking to ICICI, Zerodha, and Mutual Funds Sahi Hai is good practice, not a shortcut.

Conclusion

Learning how to invest in direct mutual funds for your child does not require complex strategies or constant supervision.

With a simple SIP, a few well-chosen funds, and a long-term mindset, parents can build a strong financial foundation for their child.

Start early, stay consistent, and keep things simple — that’s the real secret.

Parents who are learning how to invest in direct mutual funds for your child should also understand the basics of long-term investing and risk management.

Before finalising funds, it helps to read our detailed guide on mutual fund investment for beginners, understand the importance of diversification in mutual funds, and learn how SIP works for long-term wealth creation.

If tax planning is a concern, exploring tax rules on mutual fund investments can also help parents make more informed decisions while building a strong financial foundation for their child.

FAQs (SEO-Optimized)

Is it safe to invest in direct mutual funds for a child?

Yes, when invested through regulated platforms and suitable funds.

What is the minimum amount to start investing for a child?

You can start SIPs with as little as ₹500 per month.

Can grandparents invest for a child?

Yes, but tax rules apply based on the investor.

Is SIP better than lump sum for child investments?

Yes, SIP offers discipline and lower market risk.

When should I stop investing for my child?

Ideally, continue investing until the goal year approaches.

Long-term investing rewards patience, not panic.